- Container prices in China saw a 47 % Y-O-Y drop from $4287 in March 2022 to $2,284 in March 2023

- Pickup charges from China to Southeast Asia saw a major slump of 84% from January to March 2023, indicating increased Intra-Asia trade

Hamburg, Germany, 17 March 2023: Asia’s shipping industry is experiencing a significant glut of inbound containers, resulting in falling container prices due to sluggish consumer demand and excess inventory, according to the March Asia container market forecaster published by Container xChange, an online container logistics company.

Grim Outlook for Container Prices Due to Uncertain Consumer Demand

Container demand has softened in the new year, following the decrease in demand in 2022, leading to a drop in container prices. In major ports across Asia, such as Ningbo, Shanghai, and Singapore, the cost of leasing and purchasing containers has dropped sharply over the past year. This means that container companies are struggling to make money and that the current situation may persist for a while.

As evidenced in the chart above, average container prices in the chart above have been on a downward trend.

For example, container prices in:

- China saw a 47 % Y-O-Y drop from $4287 in March 2022 to $2,284 in March 2023.

- Singapore, dropped by 55% from $4,338 in March 2022 to $1,951 in March 2023.

- Vietnam saw a 51% Y-O-Y drop from $4,812 in March 2022 to $2,331 to in March 2023.

- India too saw a Y-O-Y price dip of 50% from $4,237 in March 2022 to $2,127 in March 2023.

- Thailand saw a 46% Y-O-Y drop from $3,727 in March 2022 to $1,992 to in March 2023.

- Malaysia also saw a 42% Y-O-Y drop from 3,562 in March 2022 to $2,046 to in March 2023.

- Indonesia saw a 40% Y-O-Y drop from $2,793 in March 2022 to $1,682 to in March 2023.

State of Container Availability vis-a-vis Consumer Demand; Rise of Blank Sailings, Expensive Container Repositioning among other maritime disruptions

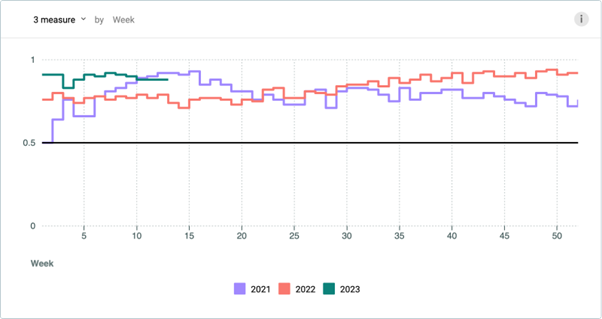

As consumer demand started to plummet in the US and EU, outbound containers started to decline and inbound containers started to rise in Asia, leading to a higher Container Availability Index (CAx) value.

The Container Availability Index (CAx) has reported a larger value for ports in China compared to 2019, 2020, 2021, and 2022, indicating a significant container excess in China.

The CAx chart from Tianjin, which is presented above, provides an explanation of the current situation. The chart reveals a significantly higher CAx level in 2023 compared to the previous two years, indicating that there are more inbound containers arriving in China as compared to outbound containers.

The CAx chart from Tianjin, which is presented above, provides an explanation of the current situation. The chart reveals a significantly higher CAx level in 2023 compared to the previous two years, indicating that there are more inbound containers arriving in China as compared to outbound containers.

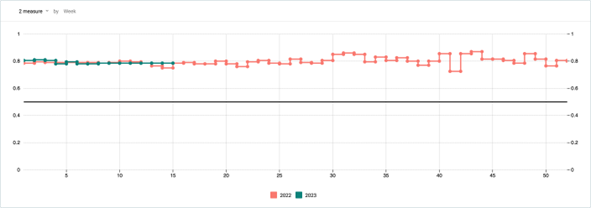

The graph above displays the CAx data for Shanghai, indicating a significant increase in the number of inbound containers at the port in 2023, as well as in 2022 by week 40. This can be attributed to the decline in demand, causing outbound containers to decrease and inbound containers to rise, resulting in a higher CAx value.

The graph above displays the CAx data for Shanghai, indicating a significant increase in the number of inbound containers at the port in 2023, as well as in 2022 by week 40. This can be attributed to the decline in demand, causing outbound containers to decrease and inbound containers to rise, resulting in a higher CAx value.

Port Kelang, Malaysia’s CAx is static at a value of 0.8 since the last few weeks.

Port Kelang, Malaysia’s CAx is static at a value of 0.8 since the last few weeks.

Singapore’s ports’ CAx values are also toppling in the range of 0.74-0.77, well above the standard 0.5 value.

Singapore’s ports’ CAx values are also toppling in the range of 0.74-0.77, well above the standard 0.5 value.

Vietnam’s Ho Chi Minh port’s CAx is fluttering in the range of 0.65-0.75

Vietnam’s Ho Chi Minh port’s CAx is fluttering in the range of 0.65-0.75

If the number of outbound containers from Asia is low, it indicates that the main countries that import from Asia haven’t been importing as much as they usually do. This is evident in the industry as well.

‘The demand for freight or containerized trade is limited due to the absence of any significant inventory destocking in the US and EU. The uncertainty around inventory restocking in the first half of 2023 has been exacerbated by the highly uncertain consumer demand side of the picture, with the potential impact of a possible recession on consumer spending in the US and EU region. This, in turn, signals a grim outlook for the revival of container prices any time soon.’ said, Christain Roeloffs, CEO & Co-Founder, Container xChange.

The falling rates and increased CAx in some regions in Asia are indicators that there is weak container demand which is widening the pool of available containers. This may also be corroborated with the weakened consumer demand and is a bad sign for the global economy because it suggests that people and businesses are not buying and selling as much as they used to.

The ripple effects of bloated container availability have been seen most in container repositioning as it becomes even more expensive owing to the current imbalance in global trade. Idle containers at the terminals are adding to port congestion. Due to this, container yards, that earn money by loading and unloading cargo from containers, also are facing challenges because there are too many empty containers sitting idle.

In response to the excess of containers and falling demand, carriers have resorted to blank sailings since the last quarter of 2022, with almost 30% of sailings from Asia cancelled after the Chinese New Year. This includes cancellations by the three vessel-sharing alliances that entail ten of the world’s biggest container carriers.

Intra-Asia trade picks up pace; South-East Asia may not fully be a China Alternative; rather an ally

Businesses are currently assessing and launching projects to test the waters by entering fresh countries to meet their supply chain demands, as part of a China plus one strategy. The fresh port data from Qingdao Port International Co indicates a deeply integrated industrial chain among Asian countries and highlights the pivotal role that China plays in facilitating an orderly global supply chain.

Commenting on the intra-Asia trade, Christian said, “The strong economic partnership between Southeast Asia and China could provide a much-needed stimulus to the world economy, which has been struggling due to various factors such as declining global demand, geopolitical tensions, and persistent inflation. This year, shipping and port firms are considering proposals to establish additional tailor-made sea transportation routes, with Southeast Asia being a key area of interest. The cooperation between these regions could give a boost to the overall ramifications of the global supply chain.”

Pickup charges from China to Southeast Asia saw a major slump of 84% from $559 in January 2023 to $91 in March 2023, whereas a 90% Y-O-Y drop from $899 in March 2022 to $91 in March 2023. This is an evident indicator of increased Intra-Asia trade.

Pickup charges from China to Southeast Asia saw a major slump of 84% from $559 in January 2023 to $91 in March 2023, whereas a 90% Y-O-Y drop from $899 in March 2022 to $91 in March 2023. This is an evident indicator of increased Intra-Asia trade.

For more on container logistics industry developments, download the full report ‘Where are all the containers’ from here