08.09.2023

This analytical piece delves into key trends in the US consumer demand and spending behavior, examining their potential implications for container demand dynamics, particularly on the transpacific trade lane.

We have identified five primary trends – shifting consumer spending patterns, weight of consumer debt and cautious expenditure, repercussions of rising interest rates on spending behavior, dynamics of savings habits and consumer confidence, and the surge in back-to-school shopping.

Subsequently, we delve into their impacts on the container and shipping industry, addressing both general consequences and specific effects. This includes a focus on the upcoming US holiday shopping season, the broader dynamics of global trade, and an examination of the outlook for the year 2024.

Summary of trends and implication over container demand

In short term, the diminishing US consumer demand presents mixed implications for container shipping. Back-to-school shopping and temporary demand surges may boost container transportation briefly. However, the evolving US holiday shopping season, influenced by factors like inflation, rising prices, and reduced savings, could create demand volatility. Uncertain consumer sentiment may lead to demand fluctuations, affecting supply dynamics, pricing, and rates.

For the medium term, these trends suggest a shift in consumer spending patterns in the US, with consumers accumulating credit card debt due to essential purchases and rising inflation. Altered holiday shopping trends and economic constraints could further dampen container demand. Cargo types transported by containers may shift, impacting supply chains and trade routes. Evolving preferences and spending habits in the US may reduce demand for certain exported Asian products.

In the long term, the implications for container shipping become more substantial. Rising interest rates and credit card debt burden could lead to prolonged cautious consumer spending. The changing US holiday shopping season, marked by restrained spending, may persist. Long-term implications include potential disruptions to global supply chains and container demand. Reduced US imports, especially from China, pose a significant challenge to container shipping and global economies. China’s role in international markets, particularly in industries like industrial equipment and consumer electronics, may be severely affected. This may lead to manufacturing slowdowns, supply chain disruptions, and job losses.

Key trends in the US consumer demand and spending behavior

Shifting consumer spending patterns

The adjusted annualized growth of the gross domestic product (GDP) for the US was 2.4% in the second quarter of 2023. This marked an increase from the 2% growth observed in the first quarter, aligning closely with the average growth of 2.1% recorded in the last 10 years.

The substantial contribution to the ongoing expansion came from consumer spending, accounting for approximately 70% of the total GDP. In Q2 2023, there was a 1.6% year-on-year increase in spending growth. While spending showed positive trends for both goods and services, it was the services sector that played the key role in driving this growth. As per Deloitte Insights, overall consumer spending is expected to grow at 1.9% year-on-year in 2023. Consumer spending on services is expected to increase by 3.1% in 2023 and by 4.7% in 2024; however, spending on durable goods is expected to decrease in 2023.

Additionally, imports of consumer goods in US are declining since Q3 2022 due to shift in consumer spending patterns favoring essential items over non-essential goods. This has led U.S. importers to be more cautious when introducing fresh inventory.

Source: Trading Economics

Source: Trading Economics

Impact on container demand ↓

Debt burden and consumer caution

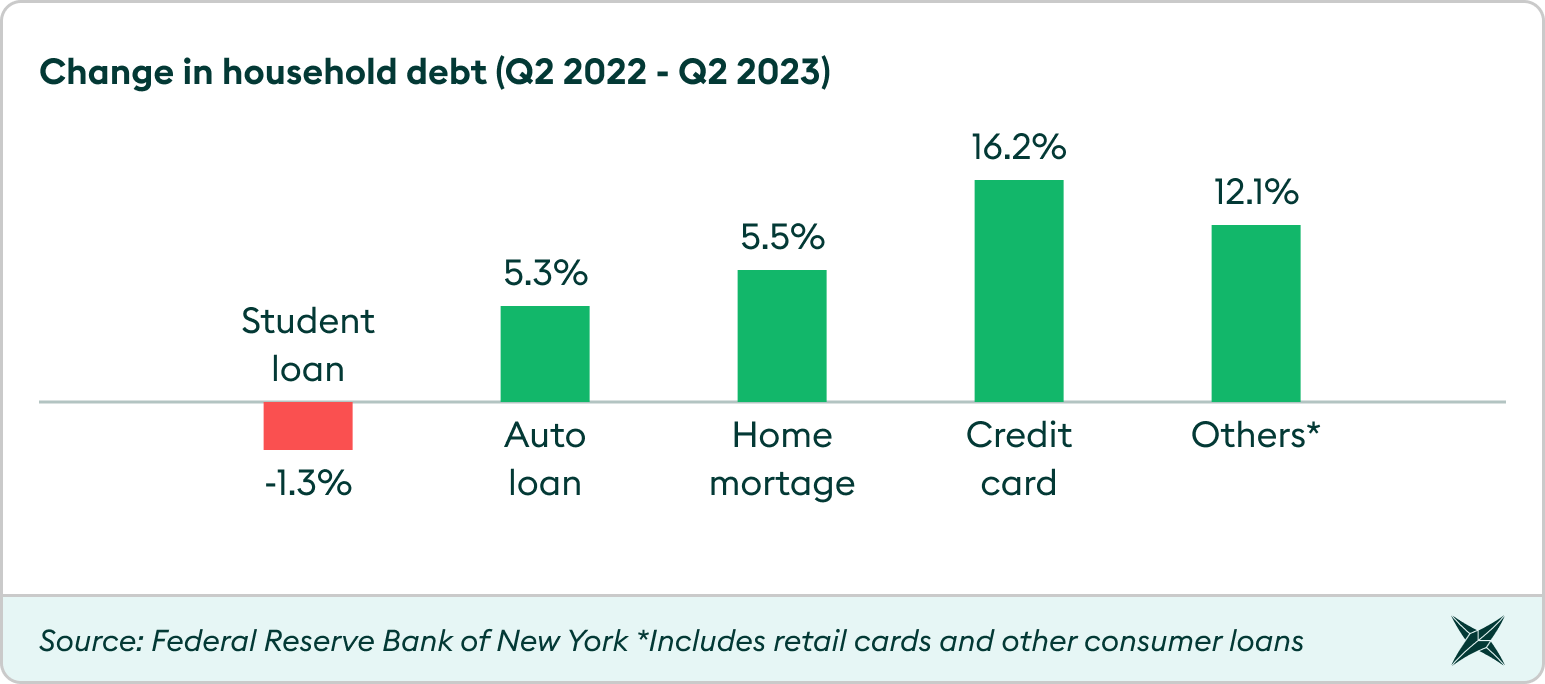

A complicating factor is the increasing credit card debt faced by Americans, which has surpassed $1 trillion, according to a recent survey from the Federal Reserve Bank of New York. The survey highlights an increase in credit card balances by $45 billion, reaching a total of $1 trillion, while the overall household debt has surged to $17.06 trillion. This increase in debt can lead to financial stress, reduced consumer spending, slower economic growth, and potential defaults. Moreover, this can also increase the use of credit cards for essential purchases rather than non-essential ones due to prolonged inflationary pressures.

Source: Federal Reserve Bank of New York

Source: Federal Reserve Bank of New York

*Includes retail cards and other consumer loans

Impact on container demand ↓

Rising interest rates and its influence on spending behavior

The surge in interest rates has triggered a notable shift in Americans’ spending behavior, particularly in relation to their credit card usage. As interest rates have steadily risen, consumers are becoming more cautious about accumulating additional charges on their credit cards. There exists an inverse correlation between consumer spending and interest rates, meaning that when interest rates are elevated, consumer spending tends to decline.

Additionally, it can also prompt consumers to boost their savings as they can potentially earn higher returns. According to the Bureau of Economic Analysis, on a seasonally adjusted annual basis, personal nonmortgage interest payments in the second quarter of 2023 have surged by 48% compared to the corresponding period the previous year, amounting to $462.6 billion now as opposed to the earlier $313.1 billion.

In essence, rising interest rates are curbing credit card spending and prompting greater savings due to increased borrowing costs and the prospect of higher returns on savings. This is demonstrated by the significant uptick in nonmortgage interest payments.

Impact on container demand ↓

Savings behavior and consumer confidence

Despite the challenges, Americans are prioritizing savings, with the second quarter savings rate as a percentage of disposable income rising to 4.4% from 3.2% the previous year. This inclination towards saving suggests a more cautious consumer approach. While increased savings could contribute to economic stability, it might concurrently limit the expansion of consumer demand for imported goods.

The recent survey by the Consumer Confidence Board reflects a marginally less optimistic consumer outlook in the US. While 21.9% of consumers considered current business conditions as “good,” down from 23.4% in the previous month, 15.2% perceived them as “bad,” remaining nearly unchanged. Expectations for short-term income growth also moderated, with 16.3% anticipating an increase (down from 18.6%), and 9.7% expecting a decrease (down from 11.8%). Notably, the perception of a potential US recession in the next 12 months saw a slight increase to 70.6% from June’s 69.9%.

Impact on container demand ↓

Back-to-school shopping surge

The National Retail Federation’s declaration of a record-breaking back-to-school shopping season indicates a temporary surge in consumer spending. The projected spending is anticipated to surge to $41 billion, a substantial increase from the pre-pandemic figure of $26 billion recorded in 2019. Additionally, individual household spending is expected to rise from $697 to $890 for this year, without accounting for inflation adjustments.

Source: NRF’s Annual 2023 Back-to-School Survey

Source: NRF’s Annual 2023 Back-to-School Survey

Impact on container demand ↑

Impact on the demand for containerized transportation

| Trend | Impact |

| Shifting consumer spending patterns | Negative |

| Debt burden and consumer caution | Negative |

| Rising interest rates | Negative |

| Savings behavior and consumer confidence | Negative |

| Back-to-school shopping surge | Positive |

Diminishing consumer demand in the US has a negative effect on demand for container shipping capacity from Asia. This drop in container demand, coupled with ample container capacity, is exerting downward pressure on freight rates and container prices. In response, effective capacity management strategies have become essential for carriers, encompassing actions like blank sailings, optimizing vessel schedules, and fleet size adjustments. These strategies address the evolving container demand-supply dynamics, mitigating the adverse effects on prices and rates. Below we will discuss about the short-term, medium-term and long-term impacts of the above-mentioned trends on the container demand.

Short-term impact

In the short term, the surge in back-to-school shopping may lead to temporary spikes in container demand. However, the changing landscape of the U.S. holiday shopping season, influenced by economic factors, including a 3.2% rise in the Consumer Price Index over the last 12 months, could affect consumer sentiment. Prices in important categories have significantly risen – groceries by 4.9%, electricity by 3.0%, and shelter costs by 7.7%. This inflation trend could lead to fluctuations in container demand, with potential spikes followed by spending pullbacks, impacting container supply dynamics. As per the Federal Reserve Bank of San Francisco, U.S. households held less than $190 billion in excess pandemic savings by June 2023. With rising interest rates, higher essential costs, and student loan deductions of around $10 billion per month starting in October, the rest of 2023 could be tough for consumer spending, generating a negative impact over the approaching holiday season.

Medium-term impact

As Americans accumulate credit card debt due to essential purchases and inflation, their spending patterns shift away from non-essential goods. Additionally, the changing U.S. holiday shopping season, driven by financial restrictions and rising costs, could reduce demand for both non-essential products and containers. This medium-term scenario might result in altered cargo types transported by containers, impacting supply chains and trade routes. Moreover, shifting consumer preferences may reduce container demand in the face of evolving economic challenges. In 2022, U.S. consumer spending on durable and non-durable goods experienced declines of approximately 4% and 1.5%, respectively, while spending on services witnessed an increase of more than 3.5%. These shifting consumption patterns in the US have the potential to significantly impact the types of products that Asian countries export. If US consumers continue to prioritize spending on services rather than goods, there might be a reduced demand for certain manufactured products and commodities that Asian countries typically export to the US.

Long-term impact

Over the long term, rising interest rates and the burden of credit card debt could continue to influence consumer spending behavior. The changing U.S. holiday shopping season, characterized by cautious consumer spending, may persist unless there’s a significant change in economic conditions. Additionally, the long-term impact on global trade dynamics, driven by reduced U.S. consumer spending on goods, can further contribute to fluctuations in container demand, potentially affecting the industry’s stability. Among the total exports from China, the US held the largest share of 16.2% in 2022, particularly in industrial equipment and consumer electronics. The decline in US consumer spending (reflected in reduced imports from China) presents a substantial threat to China: US goods imports from China — particularly in industrial equipment and consumer electronics — dropped 25% in the first half of 2023, according to the Commerce Department. This reduction in demand can lead to manufacturing slowdowns, disruptions in global supply chains, and potentially widespread job losses, affecting both China’s domestic economy and its role in the international market.

2024 Outlook

Due to longer-term factors such as inflation, increased interest rates, and a structural shift of consumer spending patterns from goods to services, cautious consumer spending in 2023 is likely to extend into 2024. U.S. households are expected to prioritize essentials over discretionary expenses, impacting demand for imported manufactured products.

This trend is likely to challenge the container market for an extended period and we don’t expect a rebound in demand within the next 12-18 months. This will likely lead to an increased imbalance in the container supply-demand dynamics, with excess containers in some regions and low demand on the transpacific route.

However, it’s worth considering potential neutralizing factors. If global economic conditions improve, the U.S. consumer sentiment might recover, leading to a revival of demand for imported goods. Policy decisions related to trade agreements and tariffs could also influence the demand for goods and the flow of trade between countries.