18.12.2024

Supply Chain professionals expect container prices to rise in January 2025

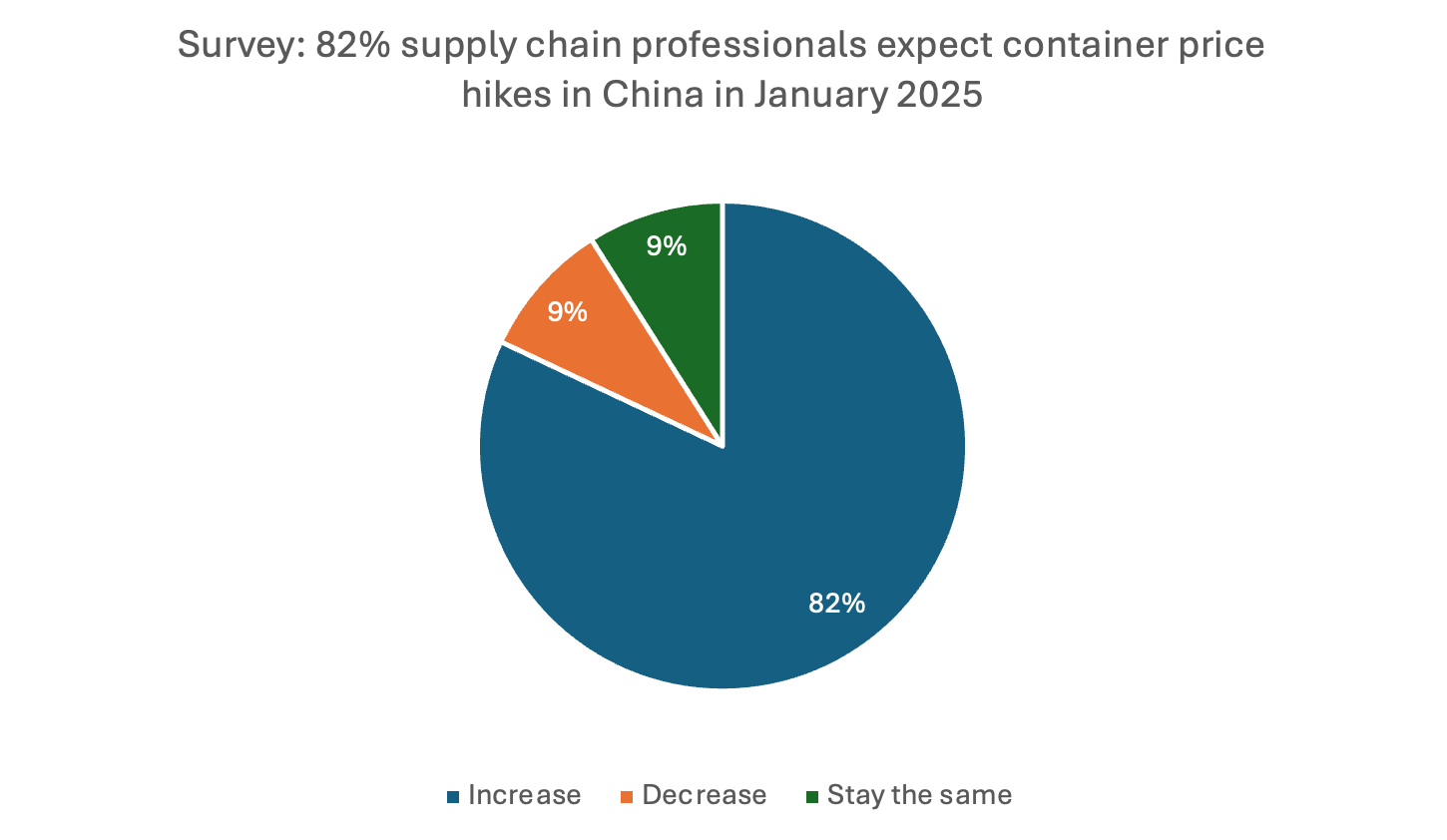

- 82% Supply chain professionals surveyed in China expect container prices to rise in January 2025

- Industry participants preparing for three key disruptions next year – ‘Tariffs implications’, ‘Geopolitical risks and war implications’ and ‘structural overcapacity’, which could keep rates volatile and market uncertain

Hamburg, 18 December 2024 – Container xChange’s latest China Market Update provides critical insights into container price trends and industry sentiment heading into 2025. The report highlights findings from xChange’s annual sentiment survey that reveals that supply chain professionals remain optimistic about container price hikes in January, citing tariffs, geopolitical risks, and structural overcapacity as their top concerns. These disruptions are expected to keep demand and supply dynamics volatile well into 2025.

Market expects container prices to rise in January 2025

Container xChange’s annual year-end sentiment survey of 900 supply chain professionals from China indicates widespread optimism about price increases in January 2025. 82% of respondents expect container prices to rise in January, driven by persistent frontloading of orders ahead of Chinese New Year closures, geopolitical risks, and potential tariff escalations.

Chart 1: xChange Annual Industry Sentiment Survey Results

Chart 1: xChange Annual Industry Sentiment Survey Results

The survey also highlights three key disruptions industry stakeholders are preparing for:

- Trump Tariffs implications

- Geopolitical risks and war implications

- Structural overcapacity, which could keep supply-demand imbalance volatile and uncertain

Christian Roeloffs, Co-founder and CEO of Container xChange, shared,

“Rising uncertainty and volatility will likely sustain container rates at elevated levels well into the Q1 of 2025. The data indicates similar holding up of rates in Vietnam, where the country is increasingly becoming a key stop along the China-U.S. trade route. Similar patterns exist in Mexico, highlighting shifts of trade flows to circumvent tariffs by leveraging trade-friendly nations with strong ties to the U.S.”

China Container Price Trends: Recovery and Stabilization

Average prices for 40ft high cube cargo-worthy containers in China have been on a gradual decline in the recent months. However, a closer look at the last 24 months reveals a steady stabilization over the past six months (July – December 2024), following a period of sharp recovery earlier in the year.

Chart 2: Average prices for 40ft High Cube Cargo Worthy containers in China

Chart 2: Average prices for 40ft High Cube Cargo Worthy containers in China

In China, the average prices for 40ft High Cube Cargo Worthy containers show a clear trend of recovery and growth from 2023 to 2024. In 2023, prices remained relatively low and volatile, with averages ranging between $1600–$2140, reflecting subdued demand and market uncertainty. By the start of 2024, prices began to rebound steadily, driven by improving demand and increased frontloading of orders to mitigate potential disruptions. Businesses pulled forward shipments to avoid risks such as the U.S. elections in November, anticipated labor strikes on the U.S. East Coast, and the possibility of new tariffs. This led to a sharp increase in prices, peaking at $3000–$3172 in Q2 2024, particularly in key markets like Ningbo, Qingdao, and Shenzhen. Prices stabilized at elevated levels through Q3 and showed slight softening by year-end, though they remained significantly higher than 2023 levels. The combination of frontloading activity, peak shipping season, and external disruptions continues to keep container prices strong amid tightening availability and supply chain concerns.

With growing tariff concerns, it becomes essential to study the growing role of markets like Vietnam and Mexico as ‘added stops’ in the US-bound shipments from China.

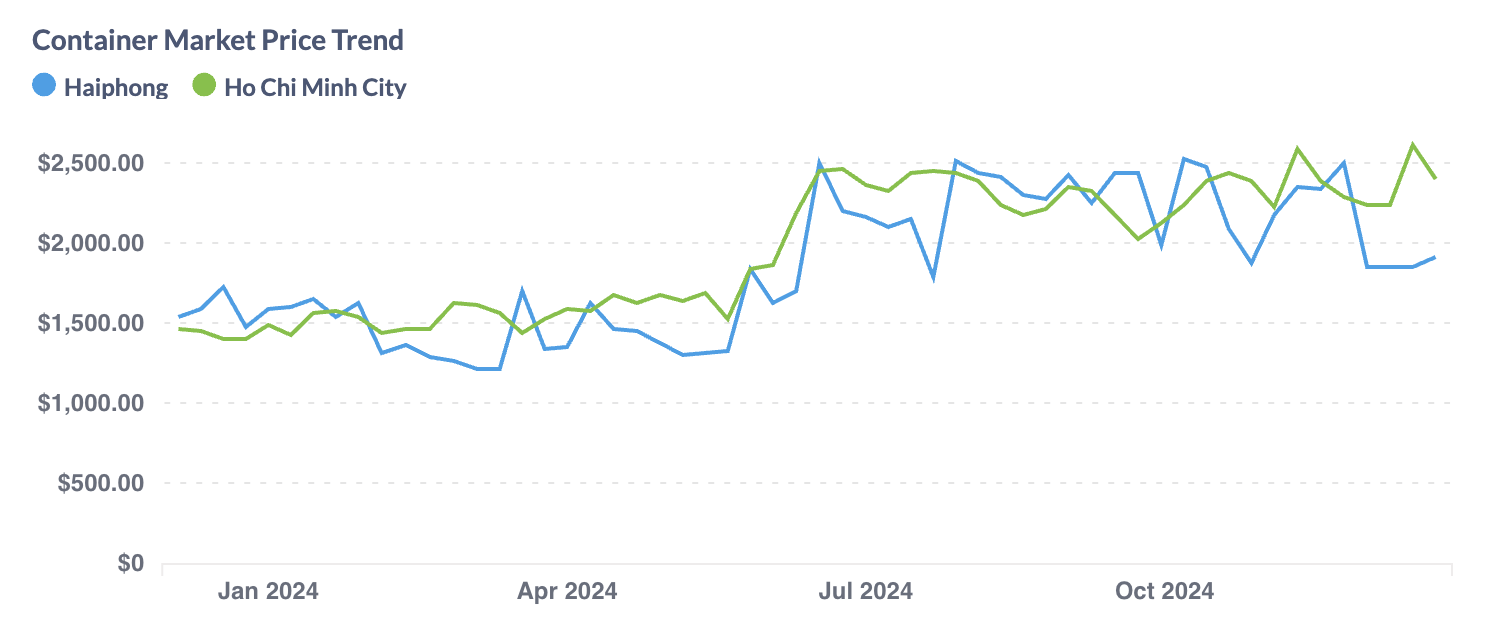

Vietnam container prices rise starkly in H2 2024

Chart 3: Average prices for 40ft High Cube containers in Vietnam

Chart 3: Average prices for 40ft High Cube containers in Vietnam

In Vietnam, average container prices surged sharply in the second half of 2024, driven by rising demand and constrained capacity. Prices in Haiphong increased by an average of 42% between March and December 2024, while Ho Chi Minh saw an even steeper rise of 66% from January to December 2024.

According to the General Statistics Office (Vietnam), Vietnam’s import-export activities continued to show positive results for the first 10 months of 2024. Cumulatively, for the first 10 months of 2024, total import-export turnover increased by 15.8% year over year. China remained Vietnam’s largest import source, while the United States remained Vietnam’s largest export market.

China-Mexico-US trade route update

Mexico has free trade agreement with the US and Canada, known as USMCA. According to industry reports, over the past three years, the number of Chinese companies in Mexican industrial sites has doubled. However, Trump has threatened Mexico’s government with 25 per cent tariffs if it cannot stop the flow of migrants and drugs north.

Revival of Tariff Policies and China’s Domestic Struggles

As trade tensions between the U.S. and China escalate, tariffs are once again at the forefront of global trade policies. During Donald Trump’s previous administration, tariffs became a defining tool of the “America First” agenda, targeting Chinese imports and triggering a retaliatory trade war. Early indications suggest a similar protectionist focus under the new administration, likely escalating costs and complexity for global supply chains.

Domestically, China is grappling with declining retail sales, though industrial output shows resilience. November’s industrial production rose by 5.4% year-on-year, slightly outpacing October’s 5.3% growth, according to the National Bureau of Statistics (NBS). Policymakers are expected to implement stimulus measures to support infrastructure investment and stabilize domestic consumption amidst slowing economic growth.

“China’s economy is bracing for a slower pace of growth in 2025, as increasing trade tensions with the U.S. and domestic structural challenges weigh on its outlook. With U.S. tariffs likely to rise, we anticipate a decline in Chinese exports to the U.S., while trade flows pivot further toward emerging markets. However, stimulus measures could provide some relief, supporting infrastructure investment and domestic demand.” Shared Roeloffs.

Labor Strikes on January 15 2025

The growing tensions between U.S. port operators and labor unions add another layer of complexity for shippers. While automation could improve efficiency, union resistance backed by political support continues to challenge supply chain resilience. Prolonged labor disputes on the U.S. East and Gulf Coasts threaten to disrupt port operations, drive up costs, and exacerbate delays.

“For the global shipping industry, prolonged labor disputes and escalating tariffs present significant challenges for 2025,” added Roeloffs. “Stakeholders must prepare for a turbulent start to the year, as shifting trade routes and nearshoring trends reshape supply chains.”

For similar analysis, reports and commentaries, and to keep yourself updated about the macro events impacting the container logistics industry, visit Container xChange Market Intelligence Hub.