21.03.2025

China’s Container Crisis: Falling Rates and Cooling Demand Concern Traders & Lessors

Shanghai, China, March 21, 2025 — China’s container logistics businesses face mounting pressure as declining container prices and leasing rates caused by weak cargo demand strain the industry. The market is experiencing growing inventory glut, making it harder for businesses to move containers.

The insights come as part of the monthly China market update (March edition) collected from its network of industry players in China and businesses from container logistics industry.

During a recent customer event in China, numerous stakeholders highlighted a concerning build-up of containers at depots, making it increasingly difficult to move inventory.

Christian Roeloffs, CEO of Container xChange, commented: “Tariff uncertainties and the slowdown in cargo transportation have intensified inventory build-ups in China, making it difficult for businesses to clear their stocks from depots. Resultantly, we observe a continued decline in container prices and average leasing rates out of China in the month of March.”

Container Prices continue to slash in China

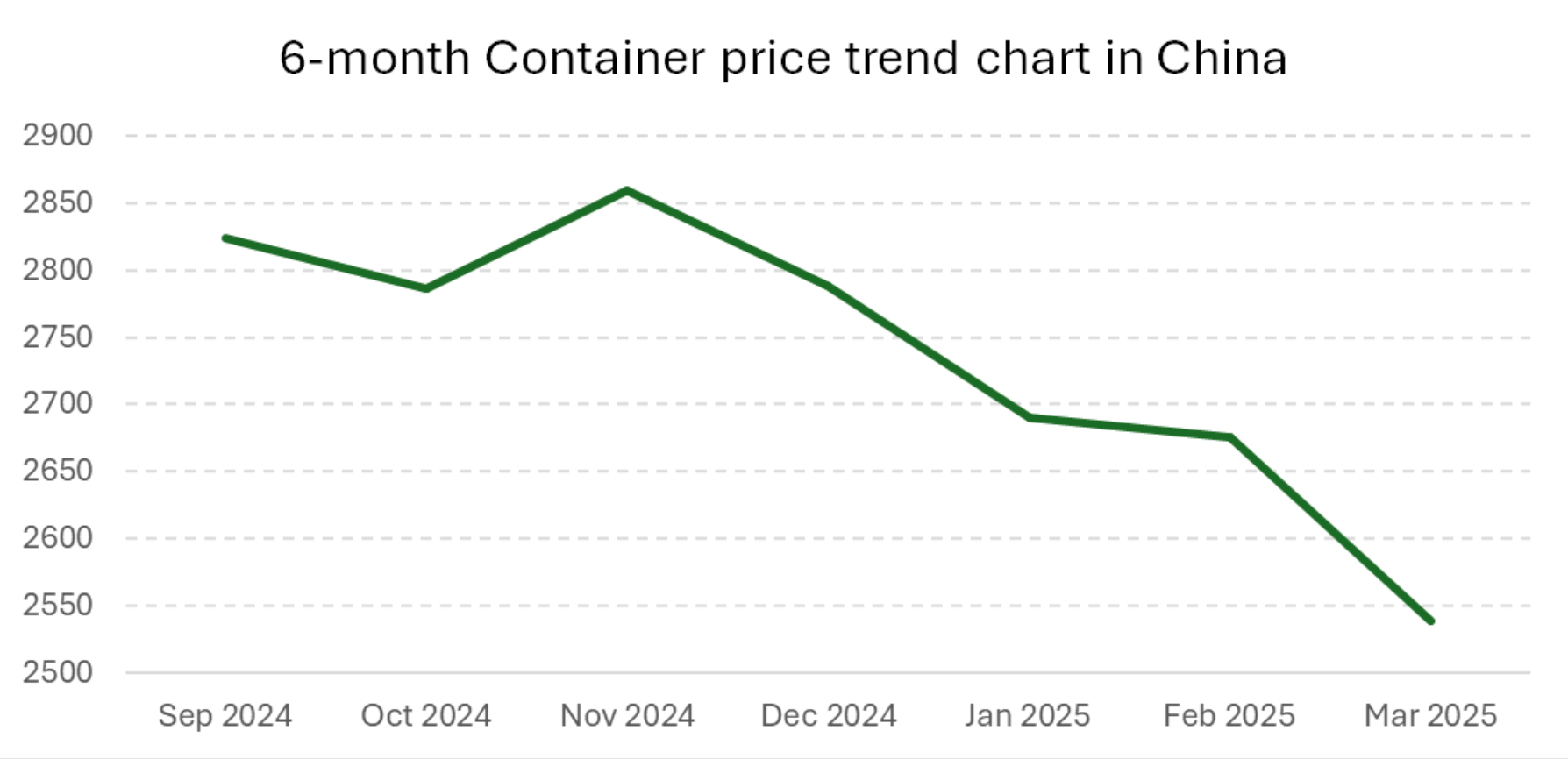

The average price of 40ft high-cube containers in China has been on a clear downward trajectory, reflecting weaker demand for container purchases. Prices have declined by 11%, from $2,859 in November 2024 to $2,539 as of March 18, 2025.

Chart 1: Average prices (In US dollars) for 40 ft high cube cargo worthy containers across locations in China between September 2024 to March 18, 2025

Chart 1: Average prices (In US dollars) for 40 ft high cube cargo worthy containers across locations in China between September 2024 to March 18, 2025

This downward trend in container pricing is not unique to China. Key container trading hubs in Asia, including Hong Kong, Singapore, Nhava Sheva, Haiphong, and Ho Chi Minh City, are experiencing similar declines, mirroring the price corrections observed in China.

- Hong Kong: The average container price in March 2025 stood at $2,632.5, down from $2,727 in February 2025 and $2,800 in January 2025, marking a steady decline over the past three months.

- Singapore: Container prices in March 2025 were recorded at $2,202, declining from $2,300 in February and $2,435 in January.

- Nhava Sheva: The March 2025 price was $1962, down from $2,057 in February and $2,060 in January, showing a downward correction similar to other major ports.

- Haiphong: Prices dropped to $2,247 in March, down from $2,377.5 in February and $1935 in January.

- Ho Chi Minh City: The market saw a similar trend, with prices at $2,152 in March, down from $2,042 in February and $2,290 in January.

The data suggests that the container price softening seen in China is part of a broader regional trend, reinforcing the notion of market correction across Asia due to weaker demand and increased inventory build-up.

Container leasing rates decline; clear indication of demand weakening in China

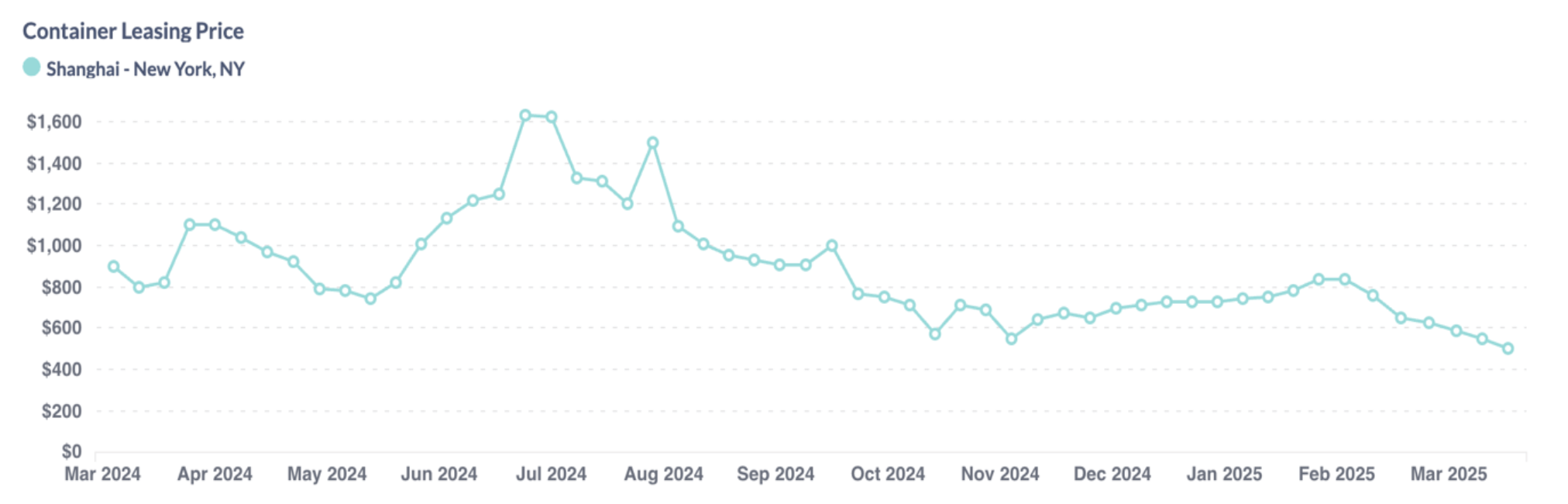

One-way leasing rates for 40ft high-cube cargo-worthy containers on key China-to-U.S. routes are experiencing a notable decline. For instance, the Shanghai to New York rate has dropped by 24%, from $720 in February to $547 as of March 17.

Chart 2: Average one-way leasing rates (In US dollars) for Shanghai to New York, for 40 ft high cube cargo worthy containers

Chart 2: Average one-way leasing rates (In US dollars) for Shanghai to New York, for 40 ft high cube cargo worthy containers

Similarly, a downward trend is observed on the Shanghai to Los Angeles route, indicating softer demand for container repositioning. This decline in leasing rates suggests an oversupply of containers in China, driven by multiple factors — a surplus of containers returning to China compared to outbound shipments and weakened freight demand affecting shippers and leasing companies.”

“What we’re seeing right now is a convergence of factors — weakened demand, tariff-induced uncertainties, and inventory imbalances.” Shared Roeloffs.

The downturn in the container market aligns with broader economic indicators in China. A notable 27.1% decline in Foreign Direct Investment (FDI) in 2024, the steepest since the 2008 financial crisis, and ongoing trade tensions with the U.S. have cast a shadow over China’s economic outlook.

“China’s container market is not just reacting to internal economic dynamics but is also caught in the crossfire of shifting global trade routes and policies,” Roeloffs explained. “As a result, container owners and traders are adopting a ‘wait and watch’ policy while the importers in the U.S. have overstocked inventories for the coming busy period.”

“The main pain point our Chinese customers are facing is the low cargo transportation demand and volume.” shared Roeloffs.

Market Outlook

As retailers and manufacturers in the U.S. rush to overstock inventories in anticipation of potential tariffs, container prices and leasing rates are expected to stay depressed in the second half of 2025. The demand from the U.S. stems from front-loading of orders rather than an actual surge in consumer demand. With no strong indications of a U.S. demand upswing, container prices and leasing rates are likely to remain under pressure unless unforeseen factors drive a rebound in consumer spending.

Port of Los Angeles, for instance, expects a 10% decline in volume in the second half of 2025, reinforcing expectations of lower demand and freight rate stagnation. Container demand decline is already evident in China, reflected in weakening rates. The ongoing accumulation of inventory further slows demand for new container movements, contributing to a market imbalance.

If a ceasefire in the Red Sea materializes later this year, further capacity loosening could push container rates even lower. Additionally, companies are increasingly diversifying sourcing away from China (e.g., Mexico, Southeast Asia), suggesting that the traditional China-U.S. trade route may not fully recover to pre-pandemic levels.

On the other hand, if interest rate cuts in the U.S. materialize, they could stimulate consumer demand and lead to an uptick in U.S. imports from China, improving container flows.

What This Means for Container Traders & Lessors

Traders:

- Expect continued price softness and potentially longer holding periods before container values stabilize.

- For traders, this reinforces the importance of focusing on short-term arbitrage opportunities rather than long-term speculative buying.

Lessors:

- With declining leasing rates, focus on regional repositioning opportunities and alternative trade routes beyond China-U.S. to optimize container utilization.

- Monitor inventory balance closely. Excess supply in China could continue putting downward pressure on leasing rates.

For similar analysis, reports and commentaries, and to keep yourself updated about the macro events impacting the container logistics industry, visit Container xChange Market Intelligence Hub.